Boomers Working Past Age 65 Are A Surprise Boost

Published Wednesday, January 15, 2020 at: 7:00 AM EST

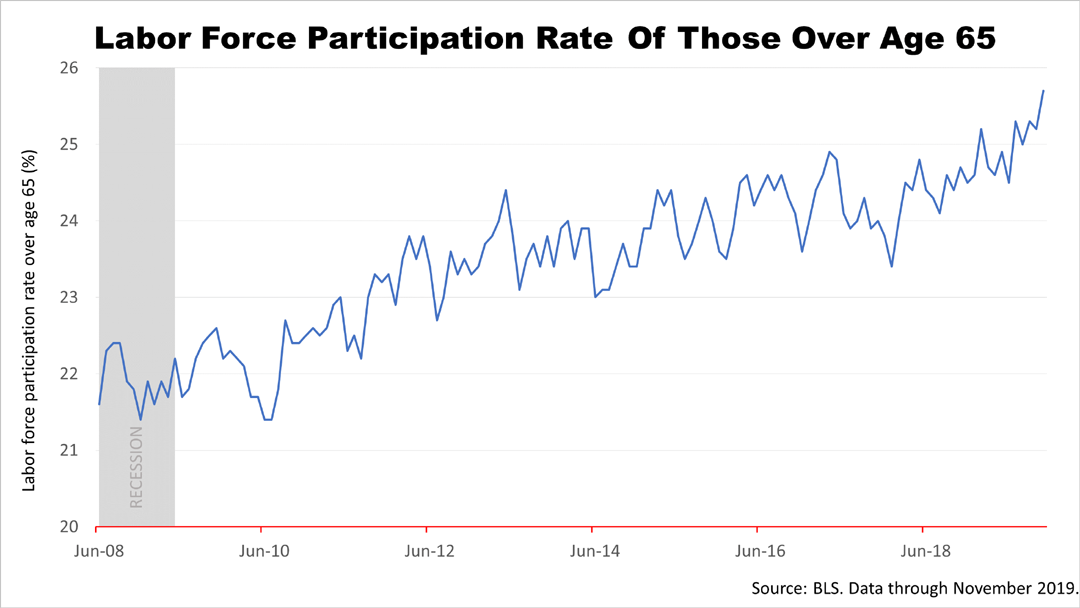

Americans over age 65 are staying in the labor force more often than expected, brightening the U.S. economic forecast and the outlook for U.S. stocks.

Turns out, the offspring of The Greatest Generation, those who served in World War II, deserve some respect, too. Baby boomers are characterized by a strong work ethic, and they are electing to work longer than government experts expected. Boomers are a key reason the economy continues to grow even as the labor market has tightened.

The Congressional Budget Office's long-term growth forecast did not count on so many boomers working past age 65. With new jobs continuing to be filled by a larger than expected number of workers in the 65-plus age group, U.S. GDP (gross domestic product) is benefitting from an unexpected boost, and it's no small thing.

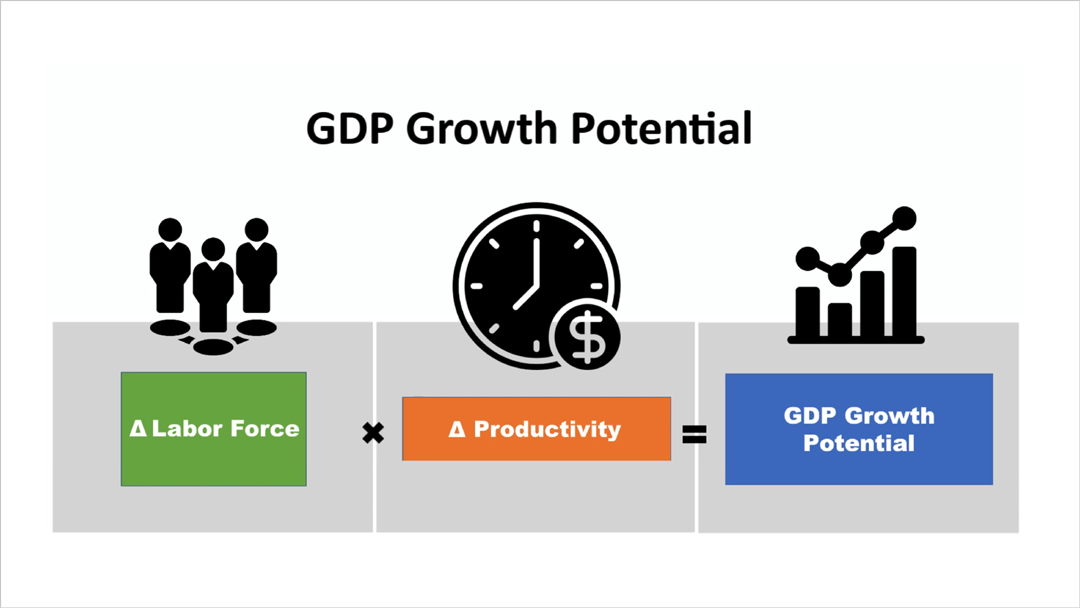

Labor force growth is a key fundamental in math economics: total growth of the U.S. economy is the product of the labor force growth rate and productivity growth. The unexpected addition of workers in the labor force improves forecasts for economic growth in the years ahead.

Historically, the economy is unable to continue to create new jobs because we run out of people to fill them. Newly-created positions drive wages higher, increasing inflation, and then the Federal Reserve makes a monetary policy mistake, which results in two consecutive quarters of shrinkage in economic activity, aka, a recession. But these times are different.

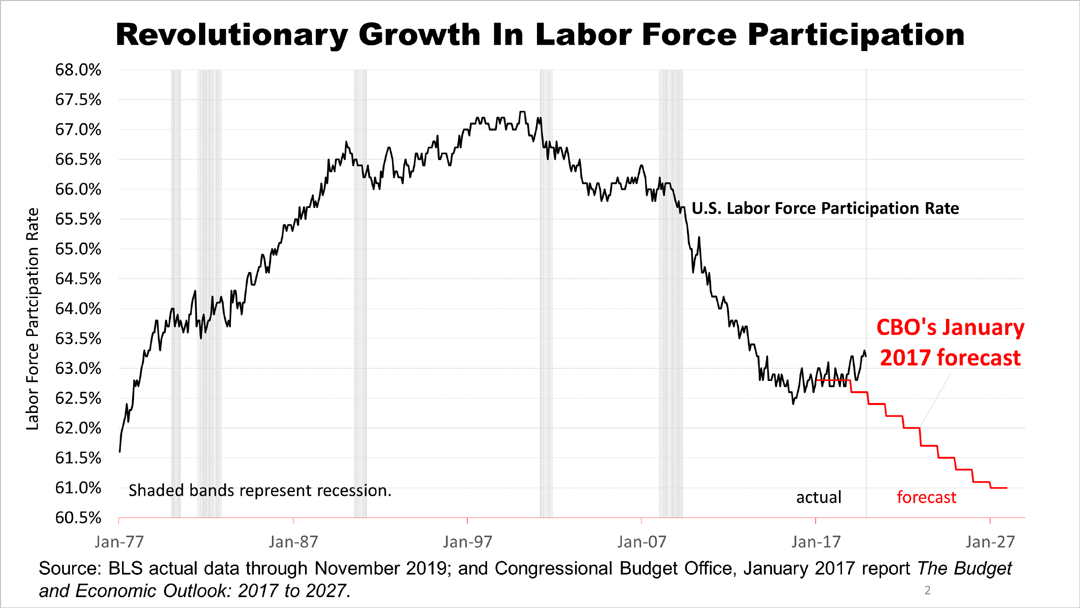

This chart captures a snapshot of Americans choosing to continue working past age 65 more often than expected by forecasters. The Congressional Budget Office, a federal agency widely recognized as an authoritative non-partisan source, in January 2017 forecasted a decline in the labor force along the lines in red. The stair-step decline in the labor force that the CBO expected is not happening! The labor force participation rate has continued to grow since 2017, when it was expected to flatten and start a long decline, and no one is certain how long the trend will continue.

The labor force participation rate is reflecting the improved longevity of Americans, which the CBO economists did not figure on in their estimates of the future. If the trend since 2017 were to continue, the U.S. labor force could contribute a totally unexpected boost of growth in consumer spending in the years ahead, and consumers account for 70% of GDP. Higher consumer spending boosts earnings of corporate America and that's good for stocks.

Let us know if you would like a special report on how U.S. demographics are affecting strategic portfolio asset allocation decisions.

This article was written by a veteran financial journalist. While these are sources we believe to be reliable, the information is not intended to be used as financial or tax advice without consulting a professional about your personal situation. Tax laws are subject to change. Indices are unmanaged and not available for direct investment. Investments with higher return potential carry greater risk for loss. No one can predict the future of the stock market or any investment, and past performance is never a guarantee of your future results.

This article was written by a professional financial journalist for Preferred NY Financial Group,LLC and is not intended as legal or investment advice.

An individual retirement account (IRA) allows individuals to direct pretax incom, up to specific annual limits, toward retirements that can grow tax-deferred (no capital gains or dividend income is taxed). Individual taxpayers are allowed to contribute 100% of compensation up to a specified maximum dollar amount to their Tranditional IRA. Contributions to the Tranditional IRA may be tax-deductible depending on the taxpayer's income, tax-filling status and other factors. Taxed must be paid upon withdrawal of any deducted contributions plus earnings and on the earnings from your non-deducted contributions. Prior to age 59%, distributions may be taken for certain reasons without incurring a 10 percent penalty on earnings. None of the information in this document should be considered tax or legal advice. Please consult with your legal or tax advisor for more information concerning your individual situation.

Contributions to a Roth IRA are not tax deductible and these is no mandatory distribution age. All earnings and principal are tax free if rules and regulations are followed. Eligibility for a Roth account depends on income. Principal contributions can be withdrawn any time without penalty (subject to some minimal conditions).

© 2024 Advisor Products Inc. All Rights Reserved.