The Big New Tax Break For Pre-Retired Professionals

Published Tuesday, October 2, 2018 at: 7:00 AM EDT

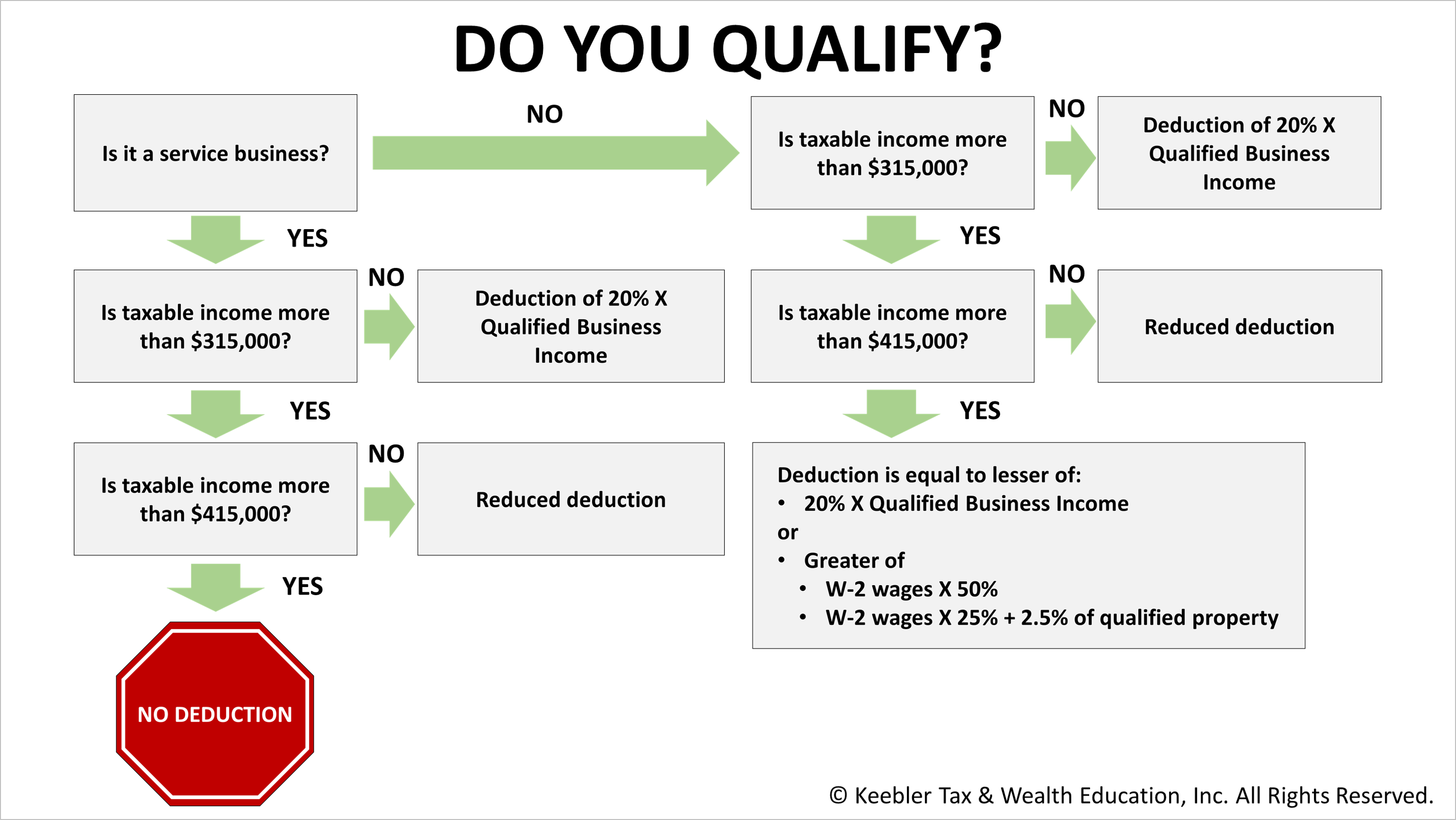

Pre-retired dentists, doctors and lawyers as well as other independent professionals may be able save tens of thousands of dollars in income taxes annually during their peak income years under the new federal tax regulations. The new rules are complex. Here are 10 things pre-retired business owners need to know about qualifying for a 20% reduction in qualified business income under Section 199(A) of the new Internal Revenue Code:

1. Sole proprietors, LLCs, S corps, partnerships and other pass-through entities qualify.

2. Real estate and rental business income — including self-rentals — may qualify.

3. Some businesses are specified as ineligible and you may need a professional to determine if you qualify.

4. Service-business owners could get a deduction on 20% of their income, subject to income limitations.

5. A business owner with $315,000 in taxable income owes tax on only $252,000 — saving more than $12,000 of income tax.

6. If you are married filing jointly and have more than $315,000 of income, the 20% deduction is subject to a phase-out. The phase-out begins at $157,500 for single filers.

7. If you have more than $415,000 of income from the service business, the 20% deduction is eliminated ($207,500 for single filers).

8. To keep your income below these thresholds, consider contributions to a defined benefit (DB) plan.

9. DB plans require you to commit to funding a defined benefit plan instead of a defined contribution plan, making them more complex.

10. A DB plan can supercharge retirement savings while minimizing your taxable income to enable you to qualify for the 20% deduction for business owners.

This article was written by a professional financial journalist for Preferred NY Financial Group,LLC and is not intended as legal or investment advice.

An individual retirement account (IRA) allows individuals to direct pretax incom, up to specific annual limits, toward retirements that can grow tax-deferred (no capital gains or dividend income is taxed). Individual taxpayers are allowed to contribute 100% of compensation up to a specified maximum dollar amount to their Tranditional IRA. Contributions to the Tranditional IRA may be tax-deductible depending on the taxpayer's income, tax-filling status and other factors. Taxed must be paid upon withdrawal of any deducted contributions plus earnings and on the earnings from your non-deducted contributions. Prior to age 59%, distributions may be taken for certain reasons without incurring a 10 percent penalty on earnings. None of the information in this document should be considered tax or legal advice. Please consult with your legal or tax advisor for more information concerning your individual situation.

Contributions to a Roth IRA are not tax deductible and these is no mandatory distribution age. All earnings and principal are tax free if rules and regulations are followed. Eligibility for a Roth account depends on income. Principal contributions can be withdrawn any time without penalty (subject to some minimal conditions).

© 2024 Advisor Products Inc. All Rights Reserved.