This Is Not Your Parents' Interest Rate Cycle

Published Wednesday, May 16, 2018 at: 7:00 AM EDT

If you're a pre-retiree, your returns on fixed income investments may be much lower than your parents' portfolio.

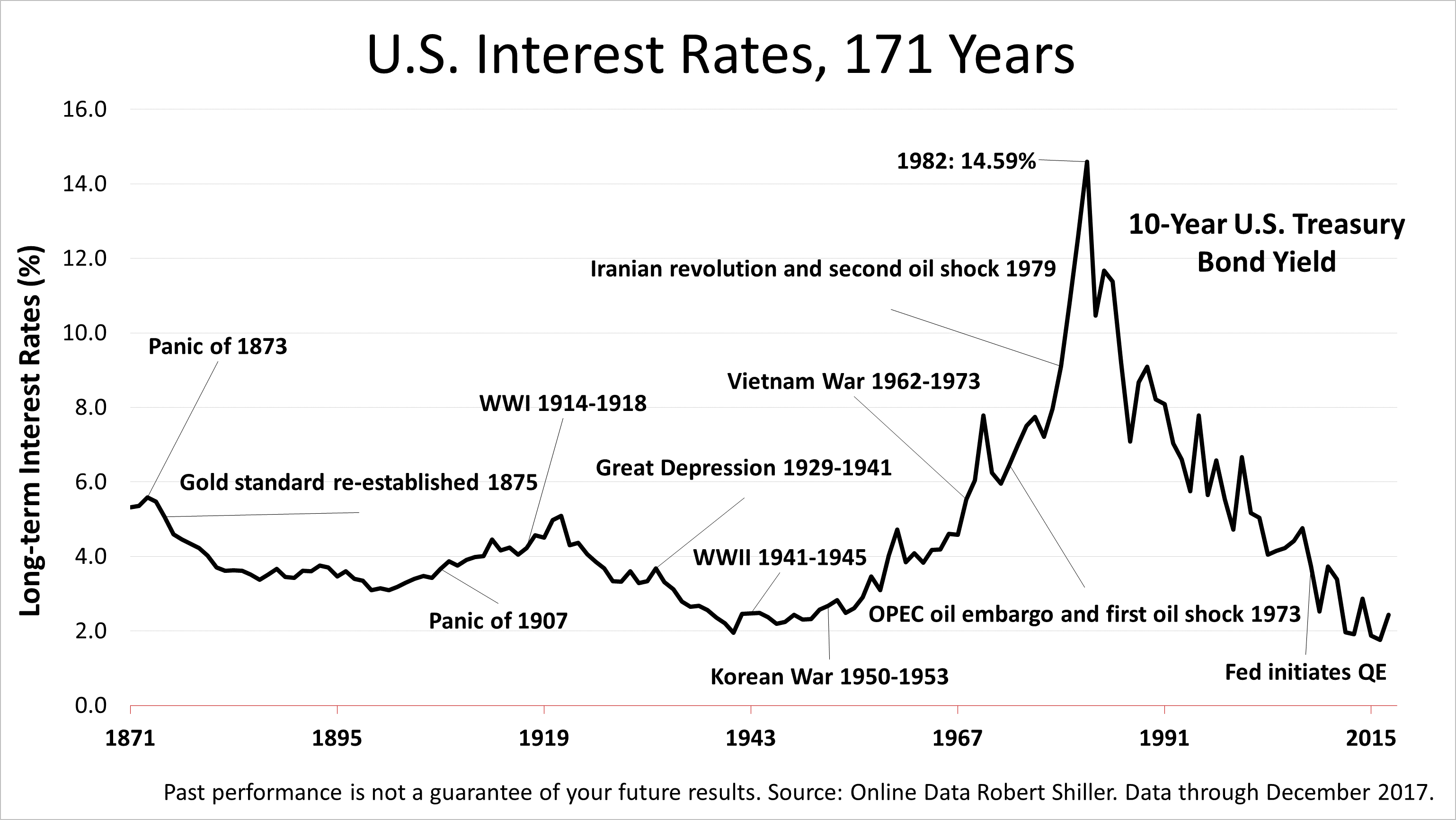

If you're over 70, you were invested during four decades marked by strong fixed income returns. From the astronomical highs of the late 1980s, rates climbed down before finally bottoming in 2017, and two generations of retirement investors enjoyed bull market returns in bonds annually for years. The next generation of retirees face an entirely different fixed income investing environment.

The last 50 years were an aberration when viewed from the perspective of the past 171 years. The rise in rates of the 1970s and 80s and the unwinding of that anomaly is behind us now, and history indicates the next decades could be characterized by 10-year U.S. Treasury bond rates of about 4%. That may be the new normal.

Past performance is not a guarantee of your future results, but we are nonetheless grateful to Robert Shiller, an economics professor at Yale University and Nobel Laurate in Economics, for sharing this historical data online. It shows that, over in the long arc of U.S. financial history, nothing like the last 50 years ever happened before the 1970s. If interest rates revert to their long-term mean, a 4% 10-year U.S. Treasury bond is a likely path in the decades ahead.

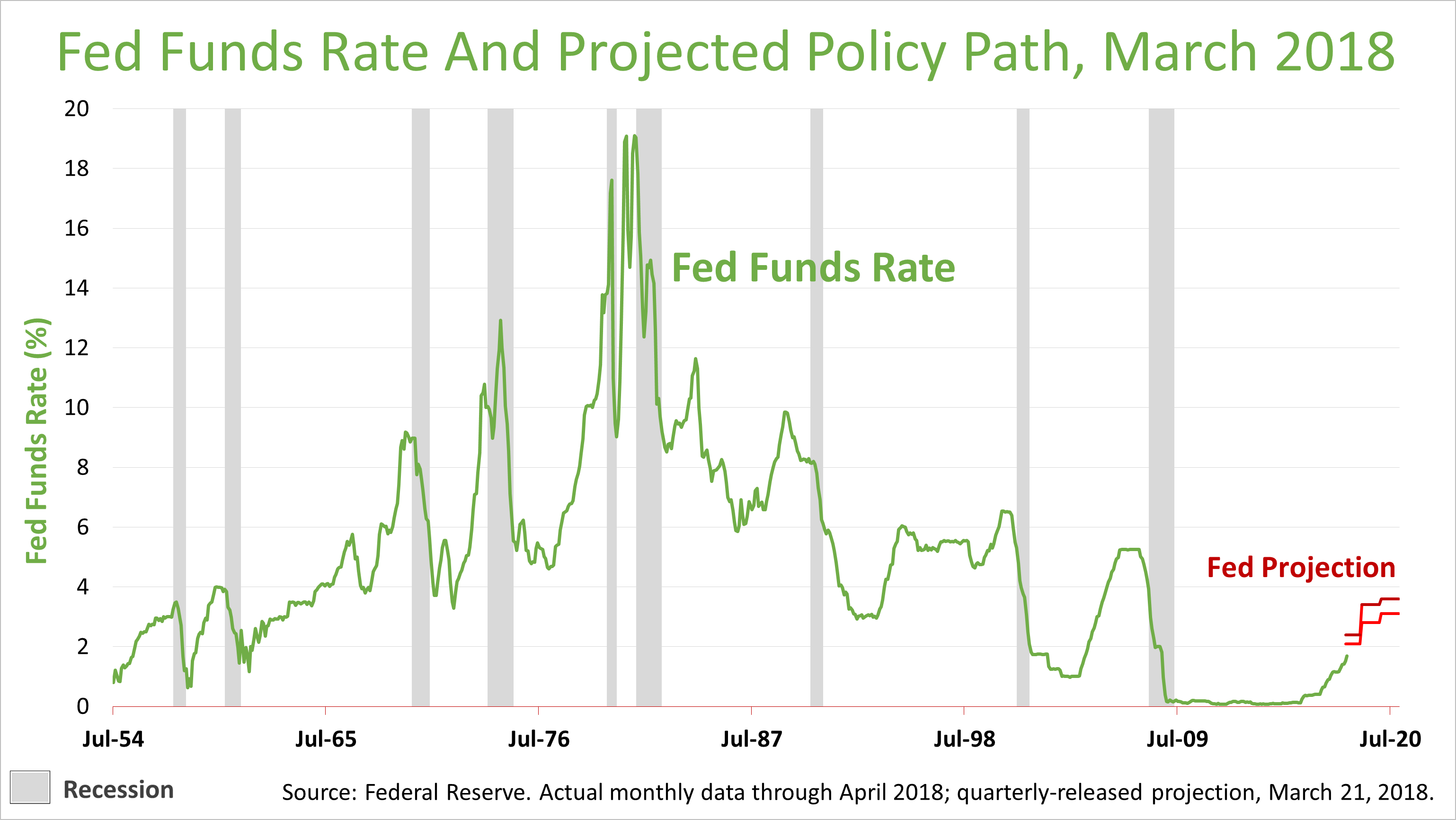

The yield on a 10-year U.S. Treasury bond, in the grand sweep of history, averaged about 4% annually. That's normal. Mortgage rates of the 70s, 80s, or 90s were abnormal. The new normal may be a 2% inflation rate and a 10-year bond yield of 4%. That's what the Federal Reserve Board of Governors expected in the second quarter of 2018.

The point is, this is not your parents' retirement savings environment. Economic fundamentals are different. If you learned about investing from your parents or invest based on what's worked in the past, the future may not be much like the recent past but instead like the distant past. This is the kind of fundamental analysis you get from a real financial professional. This is the kind of analysis you can expect from us.

This article was written by a professional financial journalist for Preferred NY Financial Group,LLC and is not intended as legal or investment advice.

An individual retirement account (IRA) allows individuals to direct pretax incom, up to specific annual limits, toward retirements that can grow tax-deferred (no capital gains or dividend income is taxed). Individual taxpayers are allowed to contribute 100% of compensation up to a specified maximum dollar amount to their Tranditional IRA. Contributions to the Tranditional IRA may be tax-deductible depending on the taxpayer's income, tax-filling status and other factors. Taxed must be paid upon withdrawal of any deducted contributions plus earnings and on the earnings from your non-deducted contributions. Prior to age 59%, distributions may be taken for certain reasons without incurring a 10 percent penalty on earnings. None of the information in this document should be considered tax or legal advice. Please consult with your legal or tax advisor for more information concerning your individual situation.

Contributions to a Roth IRA are not tax deductible and these is no mandatory distribution age. All earnings and principal are tax free if rules and regulations are followed. Eligibility for a Roth account depends on income. Principal contributions can be withdrawn any time without penalty (subject to some minimal conditions).

© 2024 Advisor Products Inc. All Rights Reserved.