Stocks Set New High Closing Price Amid Turbulence

Published Friday, January 8, 2021 at: 7:06 PM EST

Despite the pandemic, despite events in Washington, D.C., and despite bad jobs report this morning, stocks set a new high closing price today.

In a world of turbulence, here’s this week’s report on the numbers that drive the economy and stock market prices.

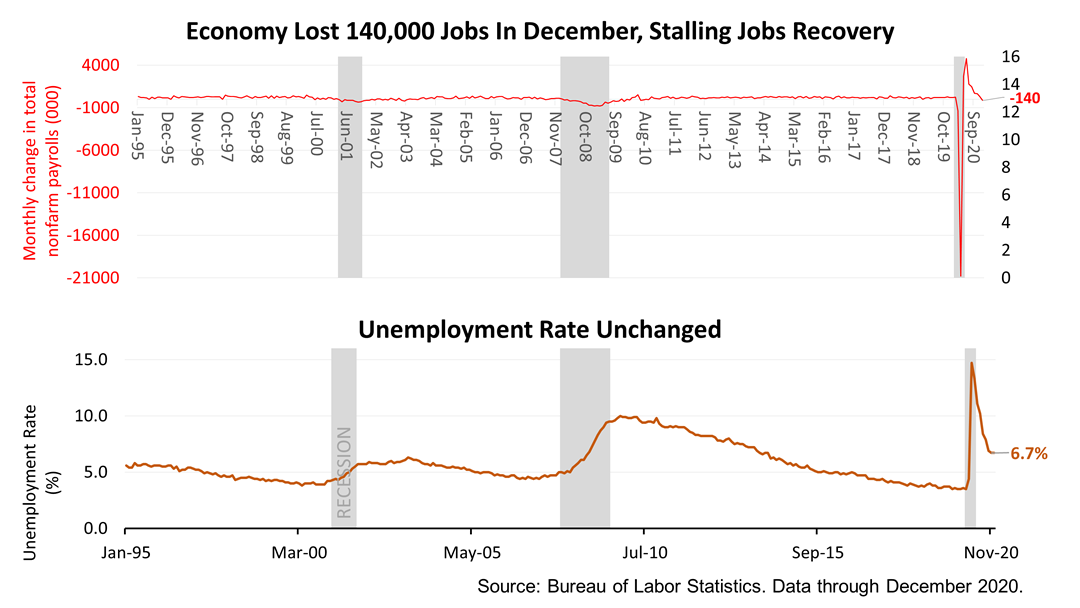

According to today’s employment situation report from the Bureau of Labor Statistics (BLS), the U.S. netted a loss of 140,000 jobs in December. That was a disappointment attributed to the worsening Covid public health crisis.

December’s job loss follows a huge gain of 336,000 new jobs in November.

BLS today revised October and November’s job gains higher by 135,000. The unemployment rate remained the same at 6.7%.

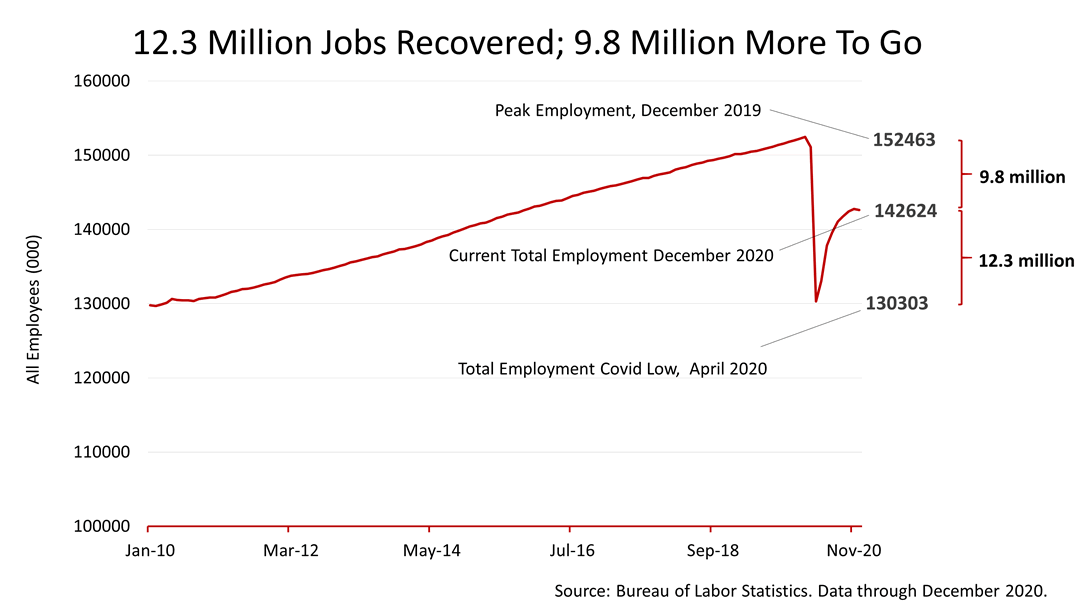

To put December’s job loss in proper context, the U.S. has recovered 12.3 million jobs since April 2020. To recover to the all-time employment peak of February 2020 – just before the pandemic hit – the U.S. will need to create another 9.8 million jobs. That would put the employment rate back to the peak of the last economic expansion, the longest in modern history, which began in April 2009. The jobs recovery to the February 2020 peak in jobs is expected to take about three years.

Despite the job situation, stocks and other investment that historically paid a premium return compared to highly-liquid 60-day U.S. Treasury bills, continued to appreciate in value.

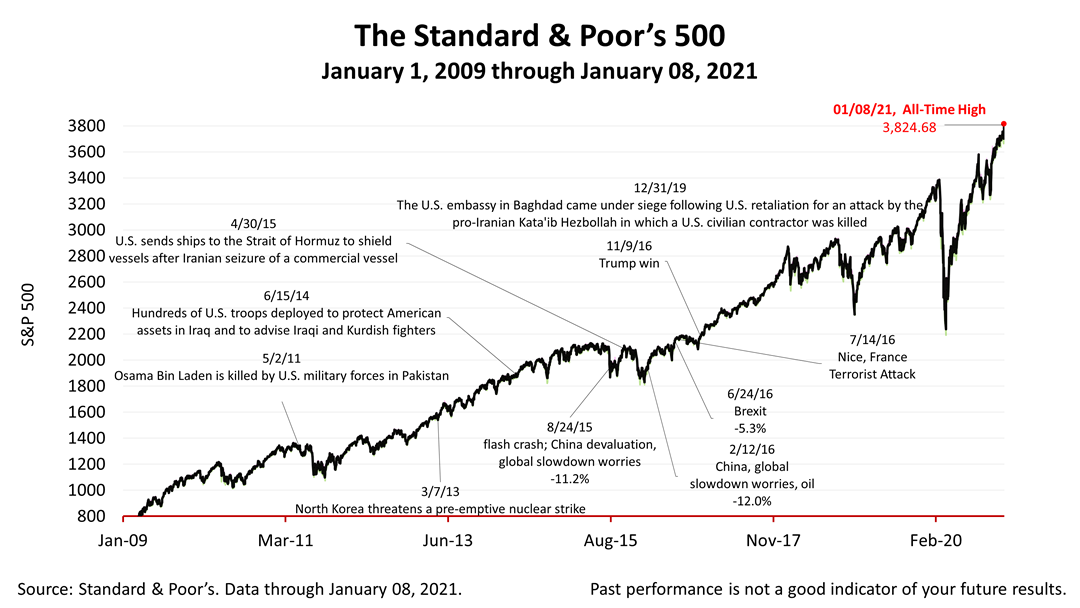

The Standard & Poor’s 500 stock index Friday set a new closing-high of 3,824.68. The new value paradigm caused by unprecedented low bond yields and low inflation has changed the traditional investment asset valuation paradigm. Please see our previous updates on this topic or contact us with questions about how the change in the relative value of bonds versus stocks might affect a portfolio invested for long run sustainability.

The S&P 500 index gained +0.55% from Thursday and +1.81% from a week ago. The stock market has gained an astronomical +52.36% from a March 23rd bear market low.

Nothing contained herein is to be considered a solicitation, research material, an investment recommendation, or advice of any kind, and it is subject to change without notice. It does not take into account your investment objectives, financial or tax situation, or particular needs. Product suitability must be independently determined for each individual investor. Tax advice always depends on your particular personal situation and preferences. The material represents an assessment of financial, economic and tax law at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources. It is not guaranteed as to accuracy, does not purport to be complete, and is not intended to be used as a primary basis for investment decisions. Any investments or strategies referenced herein do not take into account the investment objectives, financial situation or particular needs of any specific person. The material represents an assessment of financial, economic and tax law at a specific point in time and is not a guarantee of future results.

This article was written by a professional financial journalist for Preferred NY Financial Group,LLC and is not intended as legal or investment advice.

An individual retirement account (IRA) allows individuals to direct pretax incom, up to specific annual limits, toward retirements that can grow tax-deferred (no capital gains or dividend income is taxed). Individual taxpayers are allowed to contribute 100% of compensation up to a specified maximum dollar amount to their Tranditional IRA. Contributions to the Tranditional IRA may be tax-deductible depending on the taxpayer's income, tax-filling status and other factors. Taxed must be paid upon withdrawal of any deducted contributions plus earnings and on the earnings from your non-deducted contributions. Prior to age 59%, distributions may be taken for certain reasons without incurring a 10 percent penalty on earnings. None of the information in this document should be considered tax or legal advice. Please consult with your legal or tax advisor for more information concerning your individual situation.

Contributions to a Roth IRA are not tax deductible and these is no mandatory distribution age. All earnings and principal are tax free if rules and regulations are followed. Eligibility for a Roth account depends on income. Principal contributions can be withdrawn any time without penalty (subject to some minimal conditions).

©2021 Advisor Products Inc. All Rights Reserved.