Retirement Revolution Unexpectedly Is Boosting Economy

Published Friday, February 7, 2020 at: 7:00 AM EST

Friday, February 7, 2020 - Friday's news that 225,000 new jobs were created in January confirmed that the economy and stock market are unexpectedly benefiting from the retirement revolution. Yet that's not in today's headlines and likely won't be tomorrow. Here's an analysis of data released this past week that focuses on what's important to your financial well-being.

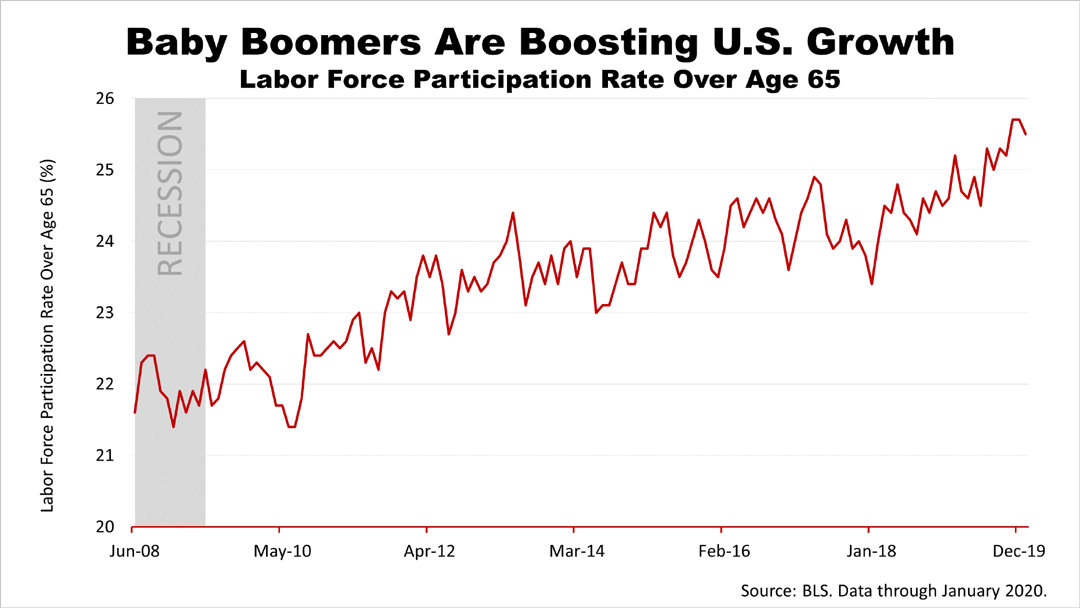

Demographers and economists never figured on so many people choosing to continue to work past age 65. It's a significant economic surprise. The fact that many more people over 65 are staying in the labor force beyond what was expected is the proximate cause of the unexpected good job numbers and recent stock market highs.

Given Friday's data, it may seem pretty obvious that the retirement revolution is boosting the economy. Yet it isn't making financial news headlines.

Actually, the better-than-expected job formation in January is only the latest in a long string of similar monthly reports over the past three years. The economy has been running near a historic low in the rate of unemployment for over three years.

In a classic American expansion cycle, eventually there are not enough people to fill all the jobs, which drives wages higher. That triggers inflation and the central bank misjudges the dynamics and makes an interest-rate policy mistake that throws the U.S. into economic decline.

While the benefit of the retirement revolution may make total sense from the data shown here, the financial press narrative last week focused on mild winter allowing construction to boom, and other activities boosting January's surprising job growth.

Today's financial news is actually a great example of why professional financial advice is so important to wealth accumulation: Even though publicly available data shows the proximate cause of the record jobs and stock reports to be the baby boomers working longer, so much was going on in the world that no press reports or talking heads on TV focused on what's truly important to managing your wealth.

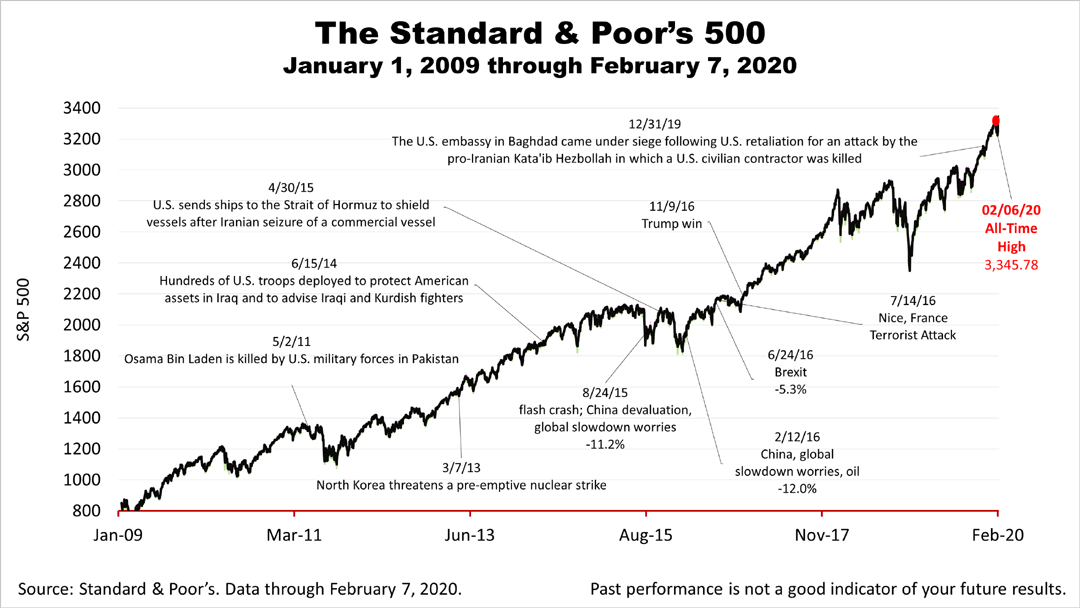

The Standard & Poor's 500 stock index, a proxy for progress, closed less than 1% off the new all-time high set on Thursday, ending the week on Friday at 3,327.71.

The Standard & Poor's 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general. It is a market-value weighted index with each stock's weight proportionate to its market value. Index returns do not include fees or expenses. Investing involves risk, including the loss of principal. Past performance is no guarantee of future results.?? Return and principal value of an investment will fluctuate, and when redeemed, may be worth more or less than their original cost. Performance statistics quoted here may be lower or higher now.

Nothing contained herein is to be considered a solicitation, research material, an investment recommendation or advice of any kind., and it is subject to change without notice. Any investments or strategies referenced herein do not take into account the investment objectives, financial situation or particular needs of any specific person. The material represents an assessment of financial, economic and tax law at a specific point in time and is not ??a guarantee of future results.

This article was written by a professional financial journalist for Preferred NY Financial Group,LLC and is not intended as legal or investment advice.

An individual retirement account (IRA) allows individuals to direct pretax incom, up to specific annual limits, toward retirements that can grow tax-deferred (no capital gains or dividend income is taxed). Individual taxpayers are allowed to contribute 100% of compensation up to a specified maximum dollar amount to their Tranditional IRA. Contributions to the Tranditional IRA may be tax-deductible depending on the taxpayer's income, tax-filling status and other factors. Taxed must be paid upon withdrawal of any deducted contributions plus earnings and on the earnings from your non-deducted contributions. Prior to age 59%, distributions may be taken for certain reasons without incurring a 10 percent penalty on earnings. None of the information in this document should be considered tax or legal advice. Please consult with your legal or tax advisor for more information concerning your individual situation.

Contributions to a Roth IRA are not tax deductible and these is no mandatory distribution age. All earnings and principal are tax free if rules and regulations are followed. Eligibility for a Roth account depends on income. Principal contributions can be withdrawn any time without penalty (subject to some minimal conditions).

© 2024 Advisor Products Inc. All Rights Reserved.