Amid Worries, New Equity Risk Premium Data Explained

Published Friday, August 2, 2019 at: 7:00 AM EDT

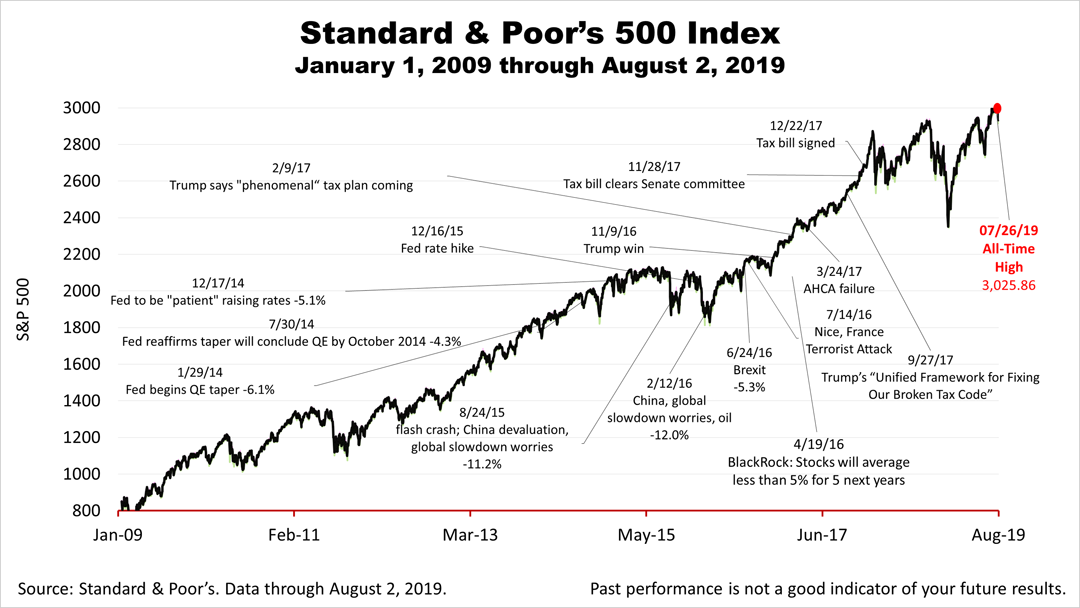

The Federal Reserve cut interest rates this past week for the first time since the 2008 financial crisis because of fears the U.S. economy was slowing. U.S.-China trade talks ended with no progress and President Trump announced additional tariffs on Chinese imports, deepening the trade war between the world's two largest economies and the chance of a global slowdown. Meanwhile, Friday's new jobs report showed continuing strength in the U.S. economy's 10-year old expansion, though slower growth could result in a cut in profit expectations in the weeks ahead, as the stock market continued to hover near its all-time high.

Amid the worries investors face, here's a reminder about this important fundamental financial concept.

A rubric of modern portfolio theory taught at colleges and universities holds that investors get paid an extra return for taking risk. The risk premium is the amount you get paid for owning a risky asset.

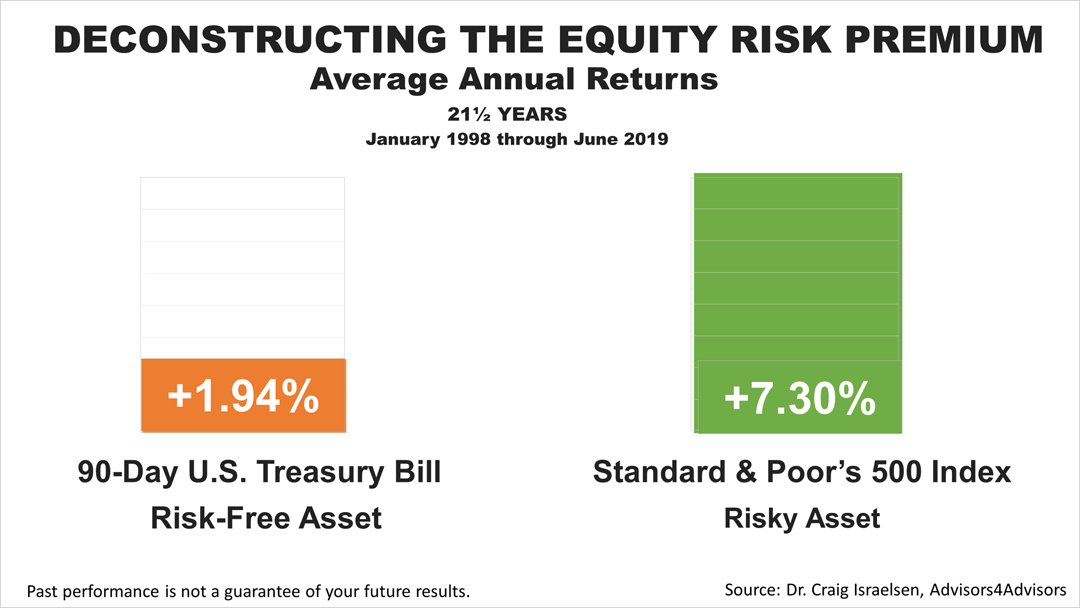

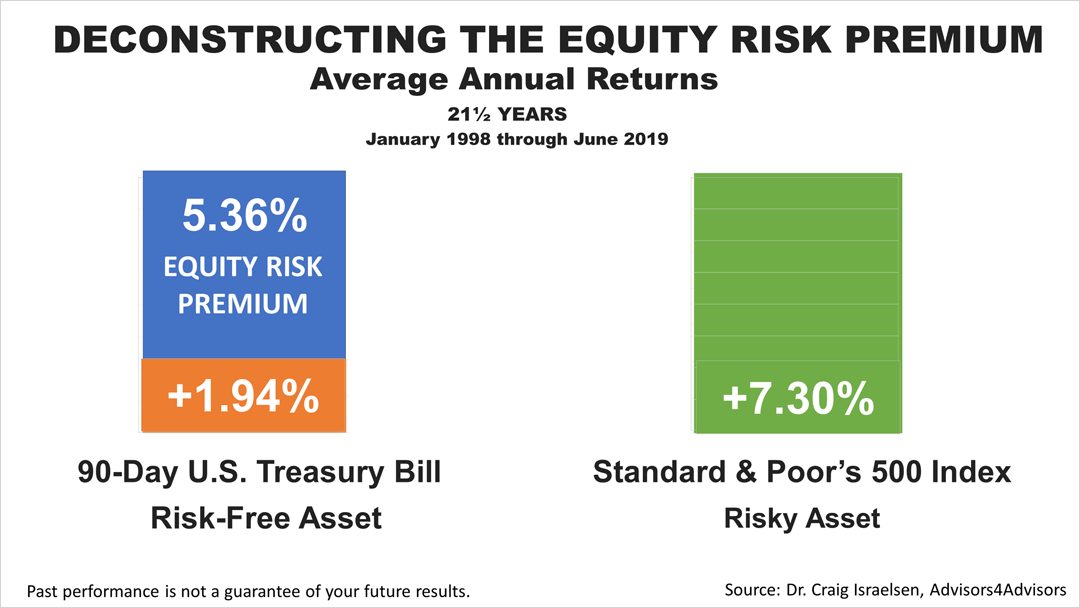

To quantify the equity risk premium, here are the numbers: Over the 21½ years ended June 30th, 2019, the risk-free 90-day U.S Treasury Bill averaged an annual return of 1.94%, compared to a 7.30% annualized return on the S&P 500 stock index, according to economist Craig Israelsen, whose research we license to share with clients and friends.

This 21½-year period encompasses two full economic and bear market cycles — the tech-bubble bursting in 1999 and the global financial crisis of 2008 — so it is an instructive period to examine.

The difference between the 7.30% average annual return on the S&P 500 index and the 1.94% return on a risk-free T-Bill is 5.36%. The 5.36% — the extra return annually averaged on equity invested in America's 500 largest publicly-held companies in the 21½-year period — is the equity risk premium.

In a time of heightened uncertainty, stock investors are tested to accept higher risk if they hope to earn a premium over less-risky Treasury Bills. That's an important financial fundamental to remember in times like these.

After closing at an all-time high of 3,025.86 last Friday, the Standard & Poor's 500 stock index of large public companies, closed about 2% lower to end the week at 2,932.05.

This article was written by a veteran financial journalist based on data compiled and analyzed by independent economist, Fritz Meyer. While these are sources we believe to be reliable, the information is not intended to be used as financial or tax advice without consulting a professional about your personal situation. Tax laws are subject to change. Indices are unmanaged and not available for direct investment. Investments with higher return potential carry greater risk for loss. No one can predict the future of the stock market or any investment, and past performance is never a guarantee of your future results.

This article was written by a professional financial journalist for Preferred NY Financial Group,LLC and is not intended as legal or investment advice.

An individual retirement account (IRA) allows individuals to direct pretax incom, up to specific annual limits, toward retirements that can grow tax-deferred (no capital gains or dividend income is taxed). Individual taxpayers are allowed to contribute 100% of compensation up to a specified maximum dollar amount to their Tranditional IRA. Contributions to the Tranditional IRA may be tax-deductible depending on the taxpayer's income, tax-filling status and other factors. Taxed must be paid upon withdrawal of any deducted contributions plus earnings and on the earnings from your non-deducted contributions. Prior to age 59%, distributions may be taken for certain reasons without incurring a 10 percent penalty on earnings. None of the information in this document should be considered tax or legal advice. Please consult with your legal or tax advisor for more information concerning your individual situation.

Contributions to a Roth IRA are not tax deductible and these is no mandatory distribution age. All earnings and principal are tax free if rules and regulations are followed. Eligibility for a Roth account depends on income. Principal contributions can be withdrawn any time without penalty (subject to some minimal conditions).

© 2024 Advisor Products Inc. All Rights Reserved.