Wealth And Economic News This Week (2-Minute Read)

Published Friday, August 10, 2018 at: 7:00 AM EDT

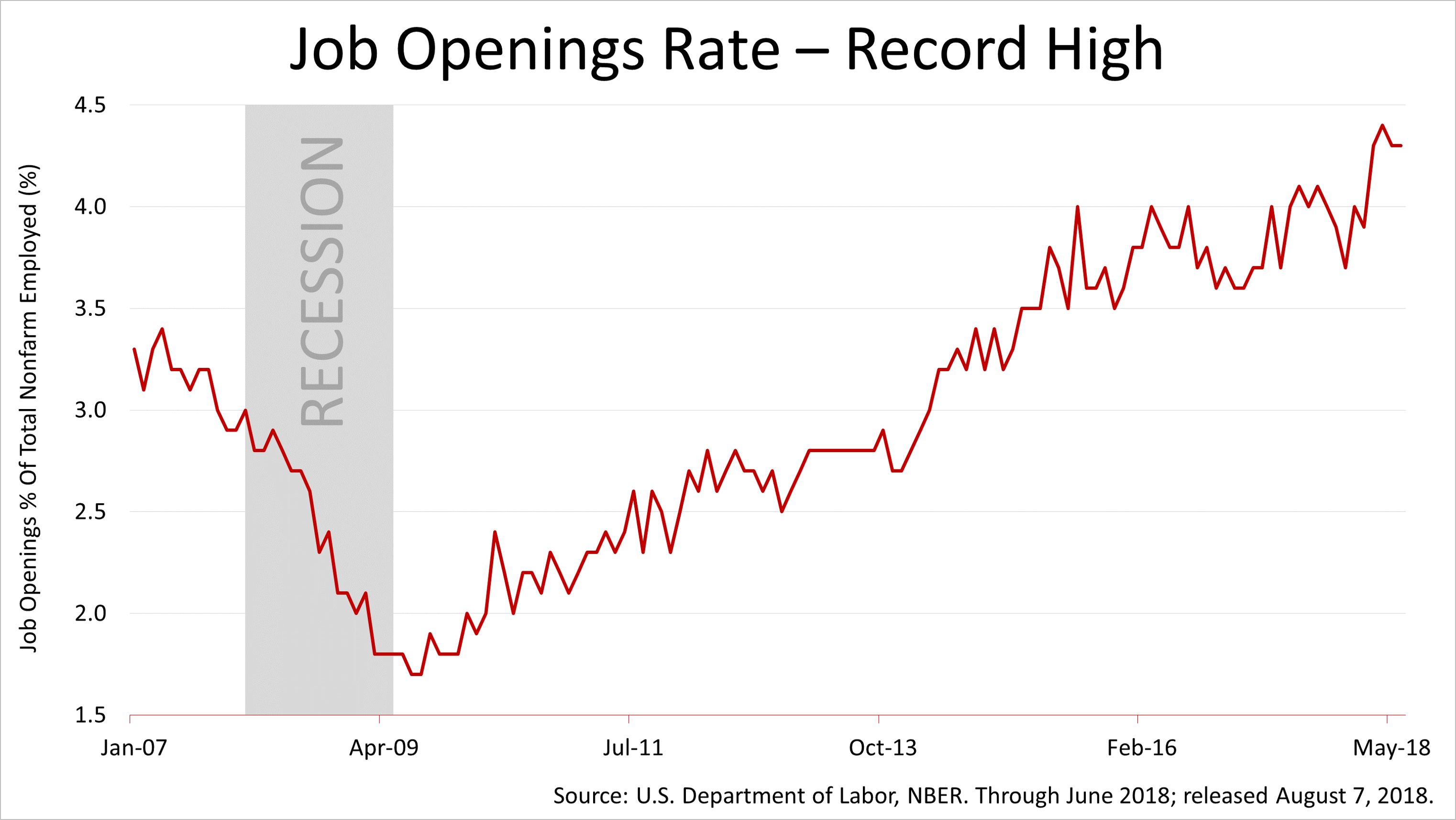

Job openings in June remained near a record high, and unemployment at a record low, while evidence of a tightening labor market grew.

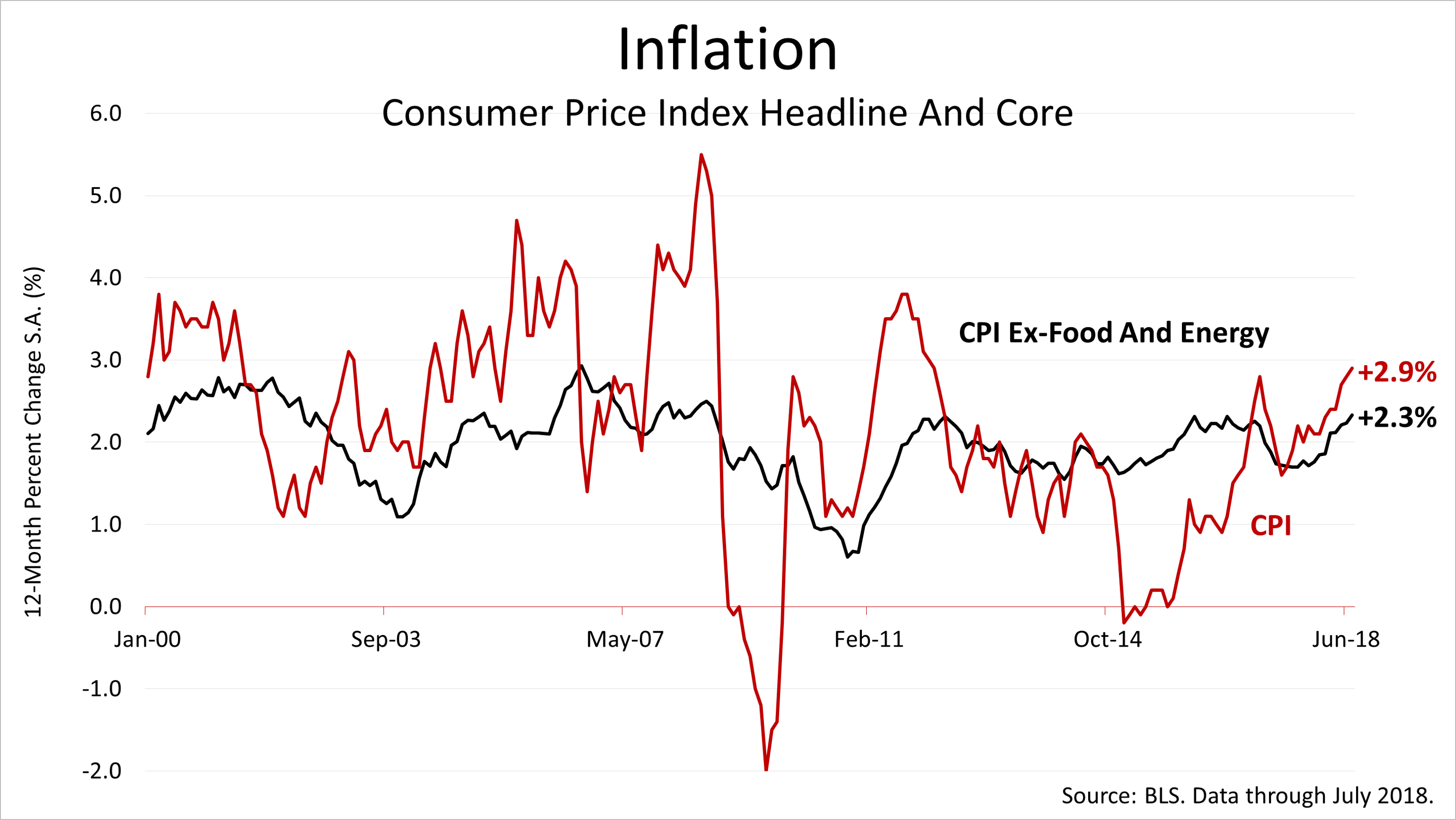

The core inflation rate, which excludes volatile food and energy prices, ticked higher in July, from 2.2% to 2.3%.

The steady rise in inflation in recent months has been expected by The Federal Reserve, and interest rate policy is expected to remain the same. The Fed has said it expects to raise rates once a quarter in 2018.

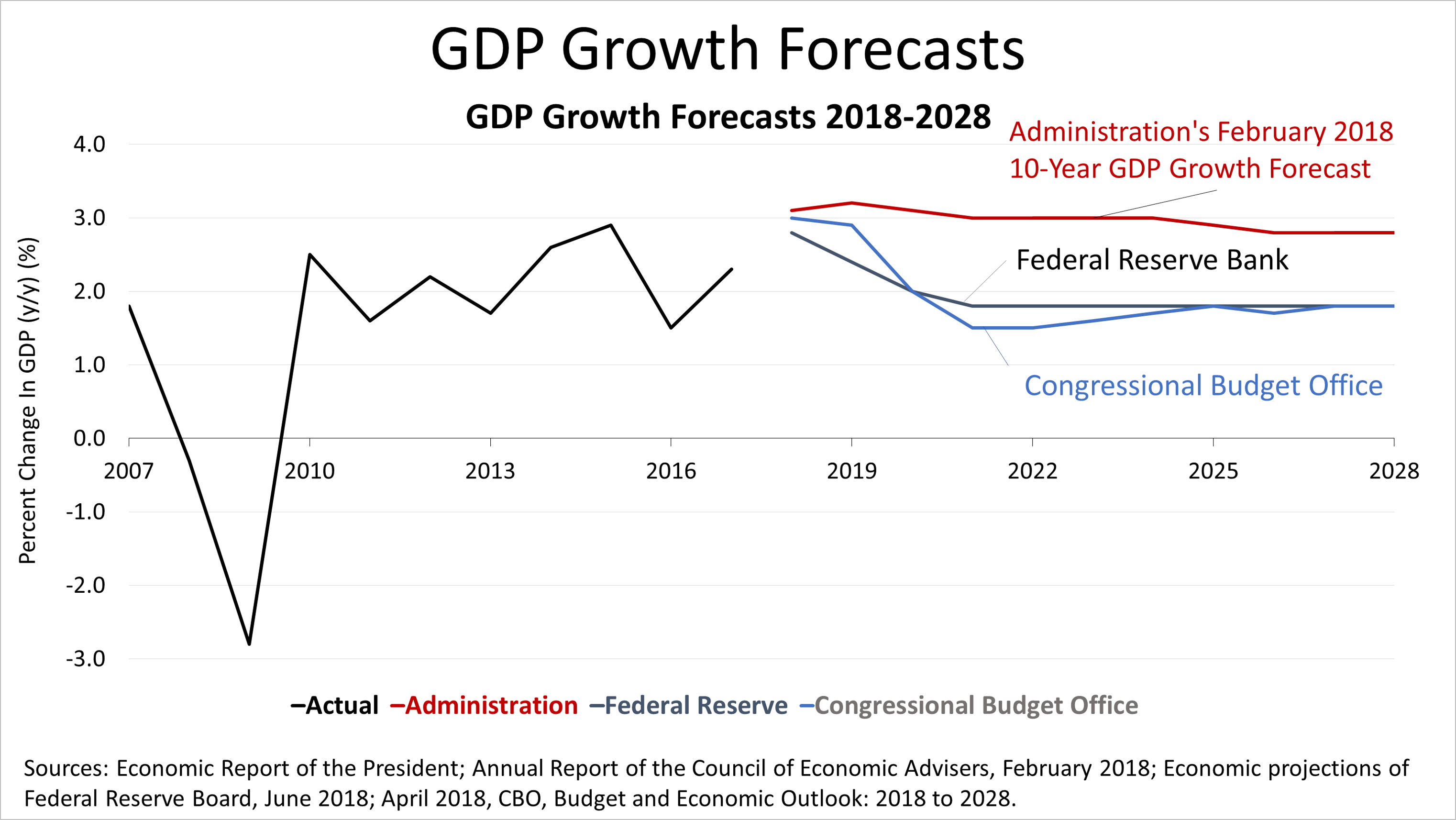

According to this month's survey of 57 economists conducted from August 3 to August 7 by The Wall Street Journal, the average growth rate estimated for 2018 increased to 3%. That was up from projections of 2.9% last month and 2.4% a year ago. The average growth rate for 2019 was 2.4%. By 2020, the average forecaster projects economic growth will slow to 1.8%, down from estimates earlier this year of 2%.

The Federal Reserve's economic forecast as well as the forecast from the non-partisan Congressional Budget Office and private economists surveyed monthly in The Wall Street Journal are all in agreement: the long-term rate of growth for GDP is about 2%.

However, the Trump administration's forecast for GDP growth in February, the most recent data available, is much more optimistic due to expectations about supply-side economics. Most economists remain skeptical about the boost in growth that will come from recent tax cuts. While the predominant view of economists is not as exciting, it is sustainable. The 110-month long expansion is, thus, poised to become the longest expansion in post-War history in July 2019.

This article was written by a veteran financial journalist based on data compiled and analyzed by independent economist, Fritz Meyer. While these are sources we believe to be reliable, the information is not intended to be used as financial advice without consulting a professional about your personal situation. Indices are unmanaged and not available for direct investment. Investments with higher return potential carry greater risk for loss. Past performance is not an indicator of your future results.

This article was written by a professional financial journalist for Preferred NY Financial Group,LLC and is not intended as legal or investment advice.

An individual retirement account (IRA) allows individuals to direct pretax incom, up to specific annual limits, toward retirements that can grow tax-deferred (no capital gains or dividend income is taxed). Individual taxpayers are allowed to contribute 100% of compensation up to a specified maximum dollar amount to their Tranditional IRA. Contributions to the Tranditional IRA may be tax-deductible depending on the taxpayer's income, tax-filling status and other factors. Taxed must be paid upon withdrawal of any deducted contributions plus earnings and on the earnings from your non-deducted contributions. Prior to age 59%, distributions may be taken for certain reasons without incurring a 10 percent penalty on earnings. None of the information in this document should be considered tax or legal advice. Please consult with your legal or tax advisor for more information concerning your individual situation.

Contributions to a Roth IRA are not tax deductible and these is no mandatory distribution age. All earnings and principal are tax free if rules and regulations are followed. Eligibility for a Roth account depends on income. Principal contributions can be withdrawn any time without penalty (subject to some minimal conditions).

© 2024 Advisor Products Inc. All Rights Reserved.