How Strategic Asset Allocation And Rebalancing Worked In The 12 Months Ended June 30

Published Friday, July 28, 2017 at: 7:00 AM EDT

A year ago, U.S. stocks were the top performers among major global stock markets. Over the past 12 months, a total turnabout occurred.

In the 12 months ended on June 30, 2016, China's stock market had sustained a loss of 21.2% and U.S. stocks were big winners among major global stock markets.

In the 12 months ended June 30, 2017, the turnaround occurred and U.S. stocks were the laggards while China roared ahead.

The turnabout offers important insight into why rebalancing and strategic asset allocation are so crucial to investment success.

In the 12 months ended June 30, 2017, China's stock market delivered a 29.6% return, compared to a 21.2% loss in the 12 months ended June 30, 2016.

The U.S. went from being the leader among major global stock markets a year ago, to being the laggard in the more recent 12-month period.

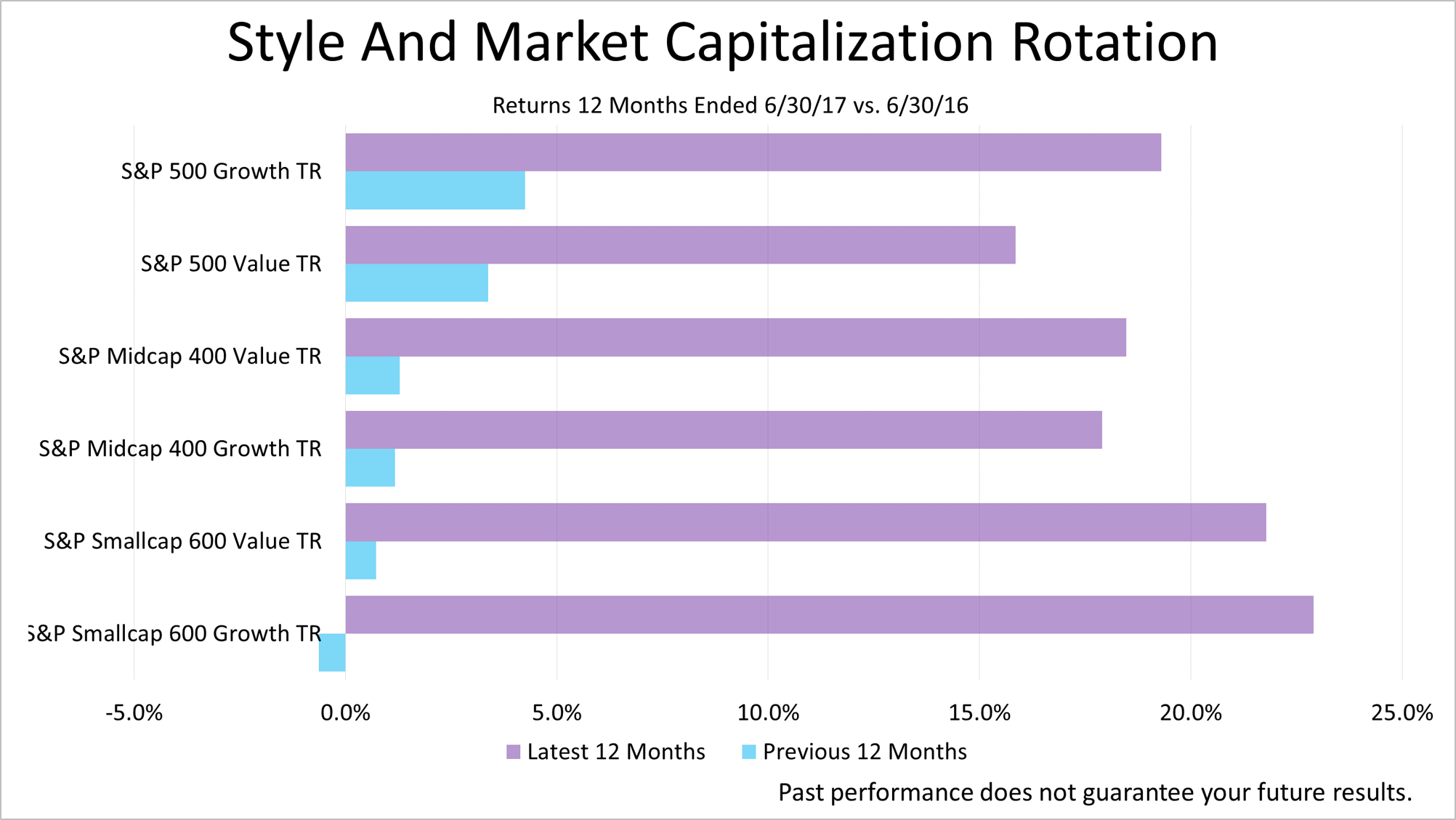

The pattern of today's losers becoming tomorrow's winners is not uncommon in investing. For example, in the 12 months ended June 30, 2016, the biggest loser among different styles of U.S. stocks was small-cap growth, which suffered a loss of six-tenths of 1%. In the more recent 12 months ended June 30, 2017, small-cap growth stocks were the biggest winners, with a 22.9% total return.

The same pattern also was seen among U.S. industry sectors. Financial stocks were the dogs of the 12-month period that ended June 30, 2016, when they lost 4.2%. But they were the darlings in the 12 months ended June 30, 2017, with a 35.4% total return.

Strategic asset allocation and rebalancing help ensure you buy lagging assets when they decline in value. So, you are prepared in case they snap back, as happened in the instances highlighted here. It's a secret of investment success because it prepares you for surprises.

With that in mind, we want to remind you that the Standard & Poor's 500 index closed on Friday at 2472.10, just a fraction off Wednesday's closing price of 2477.83, which set a new all-time high.

A change sentiment or an unexpected bad surprise could trigger a 10% or 15% plunge at any time. But last week's economic data indicated that the outlook for the economy remains positive, and the fundamentals that drive stock prices remains strong. While no one can reliably predict the stock market's next move up or down, adhering to a discipline of broad diversification, strategic asset allocation and rebalancing remains the best course for long-term investors.

We are independent financial professionals communicating at a frequency attuned to you, and you can get financial wisdom here anytime from your smartphone. Tune in to our YouTube channel for breaking news coverage and subscribe to our email newsletter.

This article was written by a veteran financial journalist based on data compiled and analyzed by independent economist, Fritz Meyer. While these are sources we believe to be reliable, the information is not intended to be used as financial advice without consulting a professional about your personal situation.

Indices are unmanaged and not available for direct investment. Investments with higher return potential carry greater risk for loss. Past performance is not an indicator of your future results.

This article was written by a professional financial journalist for Preferred NY Financial Group,LLC and is not intended as legal or investment advice.

An individual retirement account (IRA) allows individuals to direct pretax incom, up to specific annual limits, toward retirements that can grow tax-deferred (no capital gains or dividend income is taxed). Individual taxpayers are allowed to contribute 100% of compensation up to a specified maximum dollar amount to their Tranditional IRA. Contributions to the Tranditional IRA may be tax-deductible depending on the taxpayer's income, tax-filling status and other factors. Taxed must be paid upon withdrawal of any deducted contributions plus earnings and on the earnings from your non-deducted contributions. Prior to age 59%, distributions may be taken for certain reasons without incurring a 10 percent penalty on earnings. None of the information in this document should be considered tax or legal advice. Please consult with your legal or tax advisor for more information concerning your individual situation.

Contributions to a Roth IRA are not tax deductible and these is no mandatory distribution age. All earnings and principal are tax free if rules and regulations are followed. Eligibility for a Roth account depends on income. Principal contributions can be withdrawn any time without penalty (subject to some minimal conditions).

© 2024 Advisor Products Inc. All Rights Reserved.